Can I Buy a Home After Bankruptcy?

The short answer – yes!

Filing bankruptcy will disqualify you for a home loan for a while (see chart below). But sometimes not filing bankruptcy is worse. If you have a lot of past-due debts, perhaps a judgment or garnishment, or a high income-to-debt ratio, you’re not going to qualify for a loan. Read about what determines your credit score.

Qualifying for a Mortgage After Chapter 13 Bankruptcy

Sometimes, you can possibly qualify for a home loan faster if you file a Chapter 13 bankruptcy. As a general rule, if you make 12 on-time monthly payments to the Chapter 13 Trustee, you may well qualify for a home loan (FHA, VA, USDA, and others). Some loans might require you to finish the Chapter 13 and then wait two years. It depends on the type of loan.

We help clients in Chapter 13 obtain home loans on a regular basis. The big point is that filing a bankruptcy does not mean you have to wait 10 years or “forever” to get a home loan. It’s quite the opposite.

Qualifying for a Mortgage After Chapter 7 Bankruptcy

As a general rule, at least two years must pass from the date your Discharge Order was entered. Exceptions to this rule exist. The FHA home lending guidelines concerning loans to people that have filed Chapter 7 Bankruptcy state:

A Chapter 7 bankruptcy (liquidation) does not disqualify a borrower from obtaining an FHA mortgage if at least two years have elapsed since the date of the discharge of the bankruptcy. Additionally, the borrower must have re-established good credit or chosen not to incur new credit obligations. The borrower also must have demonstrated a documented ability to responsibly manage his or her financial affairs. An elapsed period of less than two years, but not less than 12 months, may be acceptable if the borrower can show that the bankruptcy was caused by extenuating circumstances beyond his or her control and has since exhibited a documented ability to manage his or her financial affairs in a responsible manner.

Additionally, the lender must document that the borrower’s current situation indicates that the events that led to the bankruptcy are not likely to recur.

Of course, you must also qualify for the loan. This includes maintaining a good credit history after filing bankruptcy, having money for a down payment, and earn enough income to make the house payment.

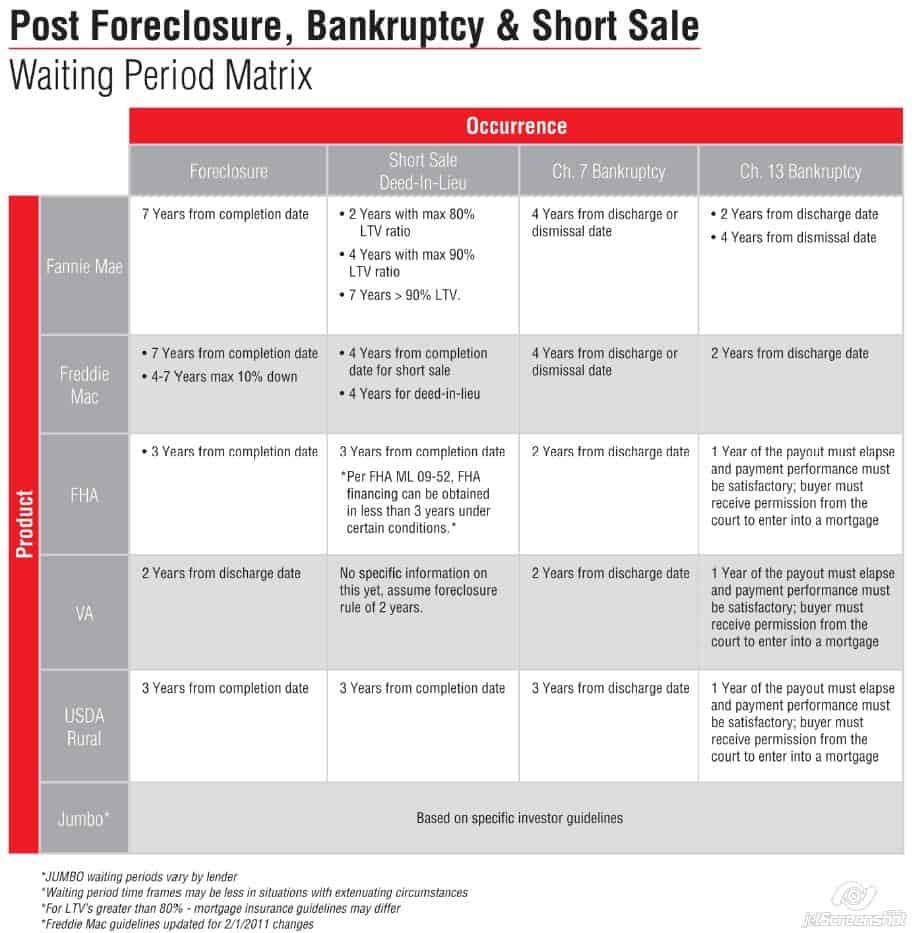

Waiting Periods

In 2018, a good friend who happened to be a mortgage loan officer provided me with this lending matrix. I believe it can still give you a decent idea of what lenders think about new home loans following a bankruptcy (Chapter 7 and 13), foreclosure, and a short sale.

To determine when you might qualify for a loan, just find your event across the top Occurrence row (Foreclosure, Short Sale, Deed in Lieu, Chapter 7 Bankruptcy, Chapter 13 Bankruptcy) and drop down until you get into the Product column with the type of loan you are seeking (Fannie Mae, Freddie Mac, FHA, VA, USDA Rural, Jumbo). The information in the intersecting box indicates when you are now might qualify for a loan (i.e., when the “occurrence” no longer disqualifies you from that type of loan).

FREE INITIAL CONSULTATION

Don’t hold off filing bankruptcy because you’re concerned about buying a home in the future. We offer a free initial consultation so you can determine if bankruptcy is the best solution for your situation, or if you have other non-bankruptcy options for dealing with your debt. We’d love to help.

A SUCCESS STORY

I recently ran into a former Chapter 7 client who received her discharge about 18 months ago. She was in a great mood, and engaged me in conversation, and thanked me for helping her and her husband through the experience of filing. She told me they were prequalified to buy a house once the two-year period passes. She said her credit score had returned to about 680. This is great news, and can happen for you as well!